Irene Asha Tirkey

Irene Asha TirkeyOct 1 - 2:30 Minutes

Going digital: payments in the post-Covid world

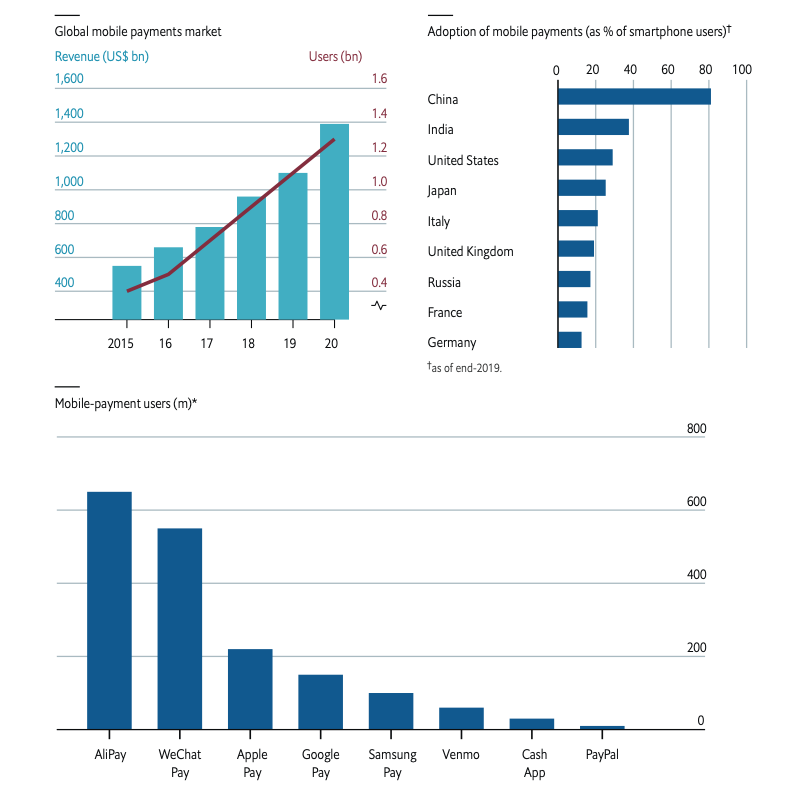

Digital payments are now compatible with mobile payments across the world. The increased rate of adoption is directly linked to access to smartphones and telecoms networks. The extreme growth in digital revenues in developing countries demonstrates the impact of the coronavirus (Covid-19) pandemic in advancing online retail sales. In contrast, governments and regulators play a vital role in facilitating the spread of new payments systems.

Hence the new change in consumer preferences and technological innovation have encouraged private-sector competition and diversity in payments. Large technology firms or big techs offer payment services as part of a much broader set of activities.

Source: The Economist Intelligence Unit

Pandemic gives regulators a unique opportunity to spur digital payments.

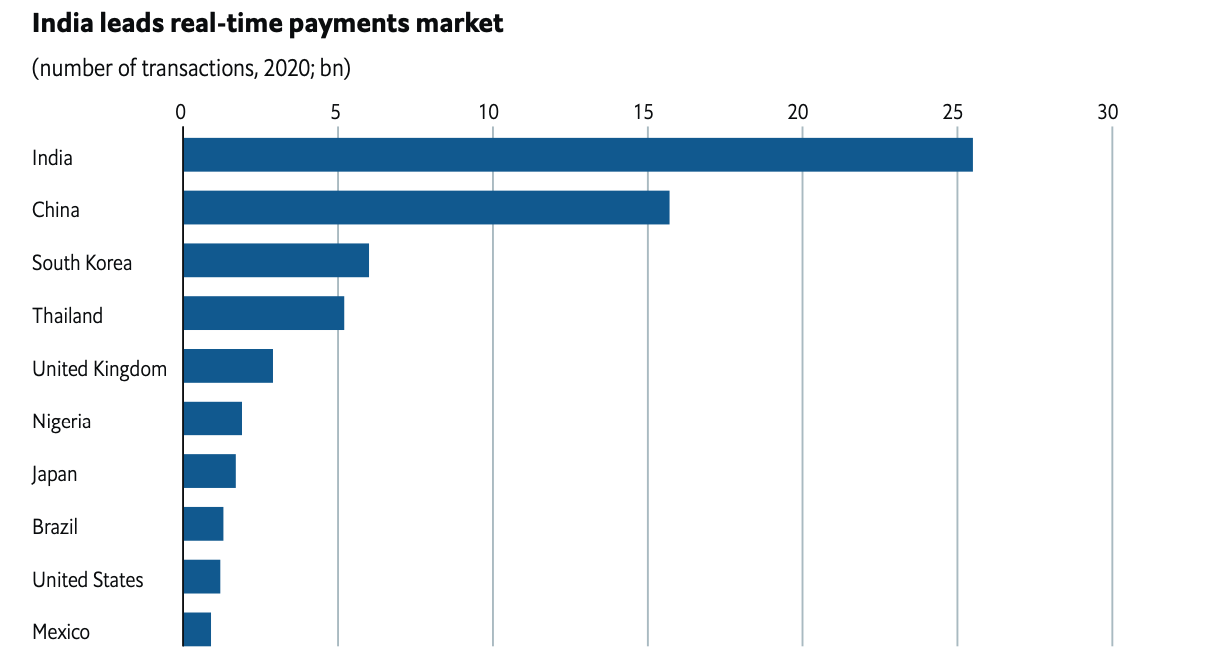

Covid-19 had its consequences which led to a change in payment infrastructure. The worldwide economies were forced to modernise their payments systems to support commerce and return economic growth. India offers a prime example of this shift. The pandemic has boosted digital payments in terms of volume and value. The prevalence of low-value payments in the Indian economy has led to the highest real-time transaction volumes. Simultaneously, the Philippines government is trying hard to achieve a cash-free society by 2025 and aims to make half of its financial transactions digital by 2023.

Fast-payment systems are transforming developing countries

Governments championing fast-payment systems indicate that they expand financial inclusion while reducing the leakage of subsidies. Now several countries have realised the benefits of digital payments and are currently building instant real-time payment platforms. However, the adoption of digital payments will mature in most countries as platforms emerge as significant distribution channels for savings and credit products. Players with diverse verticals enjoy a presence across geographies and stand to benefit by generating fees for their robust platforms from both customers and businesses. In comparison, payments operators in emerging markets are tilting towards improving their profitability.

Source: The Economist Intelligence Unit

New frontiers: central bank digital currencies

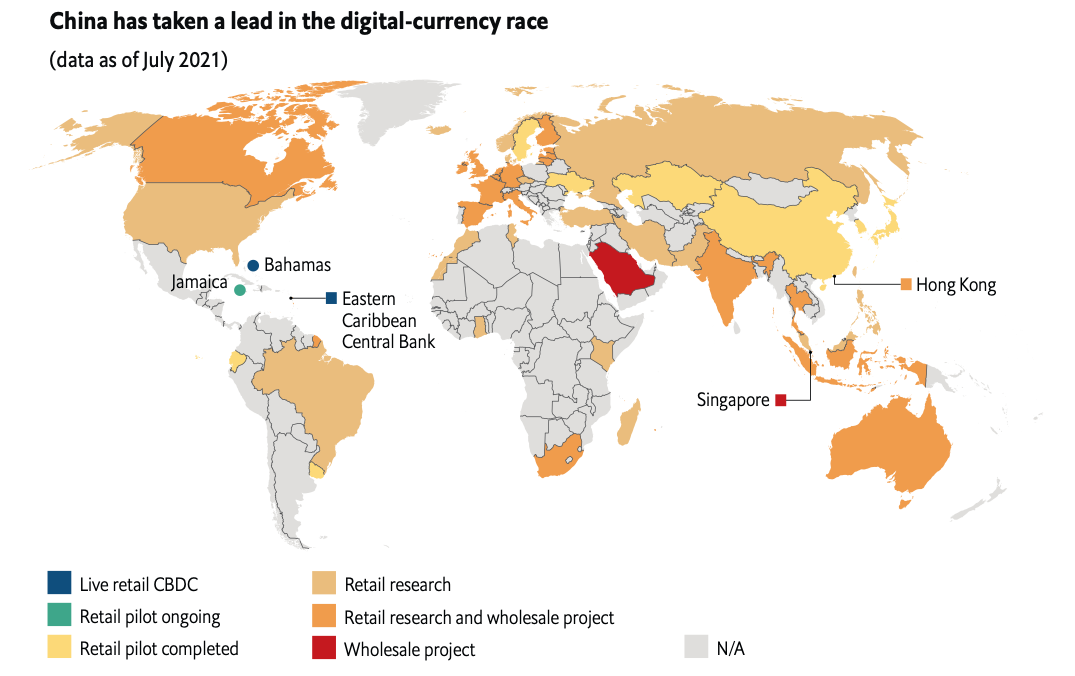

The rapid adoption of digital payments has also accelerated the launch of digital currencies. Governments aim to wrest back some control over money supplies and further facilitate the digitalisation of payment systems. Central banks worldwide advocate that these currencies should be built around digital identity, safeguarding data security and privacy, a significant criticism of cryptocurrencies.

The Bahamas, an island nation in the Caribbean, made history this year by launching the world's first digital currency, the "sand dollar". Concurrently, the other project that dominated the headlines in China's Digital Currency Electronic Payment (DCEP). Furthermore, DCEP has undertaken more than 70 million transactions worth a total of US$5.3 billion. Furthermore, visitors will have the scope to experience the e-yuan first-hand at the Beijing Winter Olympics of 2022.

Source: The Economist Intelligence Unit

In theory, a digital currency should transcend barriers between competing payment platforms, further accelerating the adoption of digital transactions. Interoperable digital currencies would also greatly facilitate cross-border payments. It removes the need for the current web of settlement mechanisms, leading to high cost and time savings while increasing ease of use. Nevertheless, most central banks will push ahead with introducing central bank digital currencies (CBDCs) to retain control of their financial systems. Therefore, the growing importance of cryptocurrencies whose values are tied to real-world currencies reduce volatility.

Transform or perish

In spite of the enthusiasm around emerging modes of payment, various sources of fear remain unaddressed. As discussed above, the absence of common regulatory standards among geographically contiguous countries is a big concern. Regulators are working towards standardising technology that allows for private firms' participation, providing an additional fillip to the digital economy. Meanwhile, traditional companies are at risk of being over-run by their digital counterparts and payment platform providers. Many have failed to create the culture of innovation that is the hallmark of the digital player. In comparison, the rest have hived off digital businesses or turned to acquisitions to remain relevant in an increasingly digitised world.

Do you want to start your money transfer operator business?

With RemitAll Software, you can remit worldwide. We take full responsibility for fuss-free transactions. Our compliance safeguards each transfer across every channel without facing any obstacles. A goal is to provide advanced technology without compromising security, quality, and innovation for your clients. Connect with us by clicking on this link https://www.remitall.co.uk.

Reading time 2:30 Minutes

Irene Asha Tirkey

Irene has completed her post-graduation in Integrated Marketing Communication from Calcutta Media Institute, Kolkata, India. Her key areas are blogging and content writing. She is in this industry for three years. Her interest areas include travelling listening to music, and painting.

Categories

Shifting Towards Digital Spell the End of Agents in Remittance. Yes or No?

May 20-2 Minutes 10 Seconds

Five Mantras For Digital Payments And User Friendly For Your Customers

May 21-2 Minutes 30 Seconds

Impact Of Remittance In Migration And Rural Development

May 27-2 Minutes 10 Seconds