Irene Asha Tirkey

Irene Asha TirkeyJune - 3:30 Minutes

Fintech Impact On Economic, Social And Financial Market

The world's reliance on technology is changing the way we live. It influences our economic, social and financial behaviour and also changing our relationship with money. While social distancing is the new normal to some degree, it exacerbates the relevance to address real situations i.e \"distancing\" such as international migration. Therefore, digital solutions act as a saviour and lead a positive transformation in people's lives.

However, access to information and communication technologies (ICT) facilitate the implementation and adoption of tech solutions. As a result, the social and economic disparities are underpinned, like income, education, and digital literacy skills. Fintech can promote inclusion and fairness in accessing digital and financial services for those traditionally left behind.

Migrant remittances

In 2019, international migration reached 272 million people worldwide, 3.4% of the global population. Moving towards prosperity, the economic prospect is the most common cause of migration. About 60% of the migrant are engaged in a remunerated activity in a foreign country. International migrant workers commonly move from Low middle-income countries (LMICs) to high-income nations in Europe, Asia and North America.

Remittances can become a significant source of income and represent an opportunity to strengthen the foundations of prosperity for migrants and recipient' communities. In 2019, remittances achieved 700 billion USD globally, with 551 billion USD sent specifically to LMICs. It was more than three times the size of official development assistance for developing countries. Moreover, it was declared the largest foreign exchange earning source and a stable financial source in receptor countries.

Remittance tagged as a financing source

Research supports that remittances can be an alternative financing source for developing countries. As a result, it increases income at national and household levels and consumes essential goods and services. Before the COVID-19 health crisis, recipients' countries received between 16% and 35% of their GDP in remittances. Moreover, these transfers were the least volatile component of balance-of-payments inflows. The impact is substantial in rural areas, where nearly half of global remittances go to 75% of the world's poor and food-insecure live.

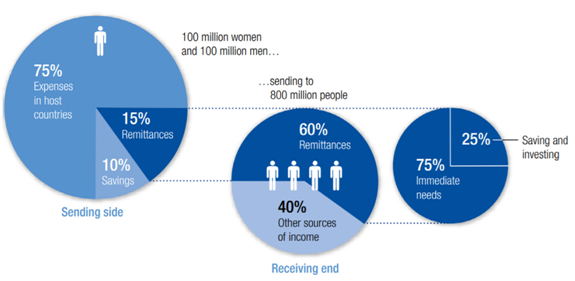

Migrant worker income distribution

Source: Fintech, remittances and migrants’ prosperity: A systematic review and exploration of the Mexican case Silvia Velasco May 2021.

Remittance Market

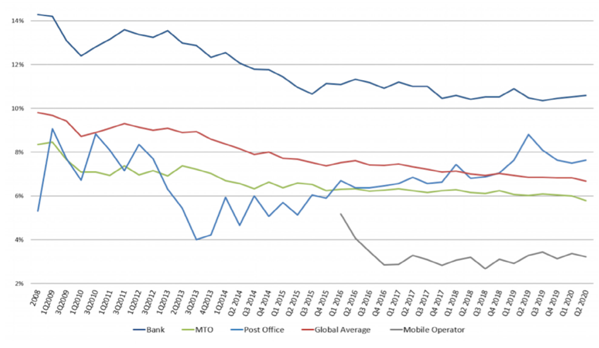

Remittance Service Providers (RSPs) play a role in defining the levels of prices and access to financial services for migrants and remittance’s recipients. So according to the report, (RSPs) worldwide charge more than 30 billion USD to process approximately 2 billion transactions annually. These transfer costs include commission fees established by the RSPs. While some providers also charge currency conversion fee for paying the remittance in local currency. In the second quarter of 2020, banks were the costliest channel for sending remittances, with an average cost of 10.57% of the total transfer. Post offices followed with 7.63%, MTO’s with 5.78% and mobile/online operators at 3.23%.

Due to extensive agent networks, MTOs lead the market with service in more than 150 countries. They represent more than 60% of the market share. Aside from transfers, most MTOs do not offer additional financial services, but they are the most used service to transfer worldwide.

Fintech based remittance

Fintech companies are on the rise because of their implications for users, financial markets, and governments. The fintech-based remittances services include innovative technology to send, receive and manage remittances. It is cheaper, convenient, relatively easy to use, secure and can improve financial behaviour. For governments, digital solutions can facilitate the effective and transparent use of public resources, reducing the “leakage” of social payments and “ghost” recipients. On the other hand, fintech’ business models can reduce operations costs and rapidly scale up access to financial services by increasing coverage. Moreover, they can address chronic financial frictions such as information asymmetries, difficulty in meeting “Know Your Customer” (KYC) and “customer due diligence” (CDD) requirements.

Average cost of remittances over time, by RSP.

Source: Fintech, remittances and migrants’ prosperity: A systematic review and exploration of the Mexican case Silvia Velasco May 2021.

The impact of fintech

Economic outcomes

The use of fintech-based remittances services has a positive impact on migrants and recipient communities’ foundations of prosperity. Moreover, many studies have supported that technology influence economic variables that increase real household disposable income. Fintech enhances the amount and frequency of remittances, as users consider the service is cheaper, easier to access and safer than other options. In addition, several authors indicate that fintech can increase investment and consumption, especially for education, health and nutrition.

Social impact

Fintech’s positive effects resulted in reducing inequalities and poverty levels. Having access to financial technology it facilitated women to managed remittances. Few economists stated that female-headed households receive significantly more remittances than their male-headed counterparts. Adding on, fintech fosters financial autonomy for women.

Financial effects

The technology boosts financial access, enhances financial behaviour by inculcating the desire to save and store money in safer channels. In some cases, it reduces savings through informal instruments such as club savings or under the mattress. Access to ICT infrastructure, mobile network, internet and broadband increases deposit accounts and loan accounts at commercial banks. Most of the authors conclude that fintech complements traditional banking and informal channels, and through competition, it can improve financial services.

Final words

As we enter an era where digitalisation is not an option but a necessity. The challenge of reducing social inequalities and improving the lives of those distanced through financial technology becomes more relevant than ever. It discovers that fintech strengthens migrants and remittance recipient’s foundations of prosperity. As a result, it increases their real household disposable income, access to better jobs, financial and digital services while shaping financial behaviour.

This information is brought to you by RemitAll Software, it is the ultimate solution for your cross border money transfer business. We take full responsibility for a hassle free experiences to enhance your customers' cross-border money transfer requirements. We can offer services to all sizes of business. To know more about us please click here https://www.remitall.co.uk.

Reading time 3:30 Minutes

Irene Asha Tirkey

Irene has completed her post-graduation in Integrated Marketing Communication from Calcutta Media Institute, Kolkata, India. Her key areas are blogging and content writing. She is in this industry for three years. Her interest areas include travelling listening to music, and painting.

Categories

Shifting Towards Digital Spell the End of Agents in Remittance. Yes or No?

May 20-2 Minutes 10 Seconds

Five Mantras For Digital Payments And User Friendly For Your Customers

May 21-2 Minutes 30 Seconds

Impact Of Remittance In Migration And Rural Development

May 27-2 Minutes 10 Seconds