Irene Asha Tirkey

Irene Asha TirkeyOct 6- 3:00 Minutes

New Start-ups are shaking up old Oligopolies

Fintech start-ups are finally getting friction in their mission to disrupt banking. Remittance is defined as smaller cross-border payments between individuals. It allows an excellent entry point for financial services. Simultaneously, the sheer charges of banks and traditional money agents have encouraged tech-savvy customers to shop around.

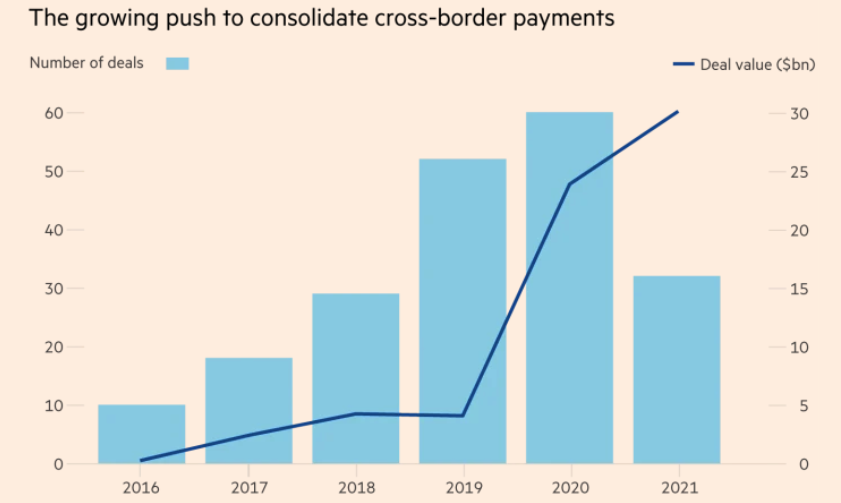

Across the border every year, the industry transfers an estimated $18tn. The landscape is highly broken down, littered with legacy businesses and their systems by creating an opportunity for well-financed acquirers to grasp rivals. The plan is to serve more extensive client bases with better technology to lessen costs while maintaining a profit.

"It is all about scale", says Ron Kalifa, a UK government adviser on fintech and chair of Network International, a payments group focused on the Middle East. The urge to consolidate triggered more than $54bn in cross-border takeovers in 2020 and 2021.

The upstart of the digital bank allows customers for fuss-free transactions

The remittance revolution challenges traditional money agents and acts as a threat to banks as well. In the past, people would drift away when somebody said they worked in remittances. But the scenario is different nowadays when they know that you are in fintech, and they get excited.

Now families back home can expect substantial remittances from expatriate earners because technology and competition can reduce costs. On the other hand, blockchain-based digital currencies enable frictionless and fully automated world payment systems.

Tech disrupt the global payments

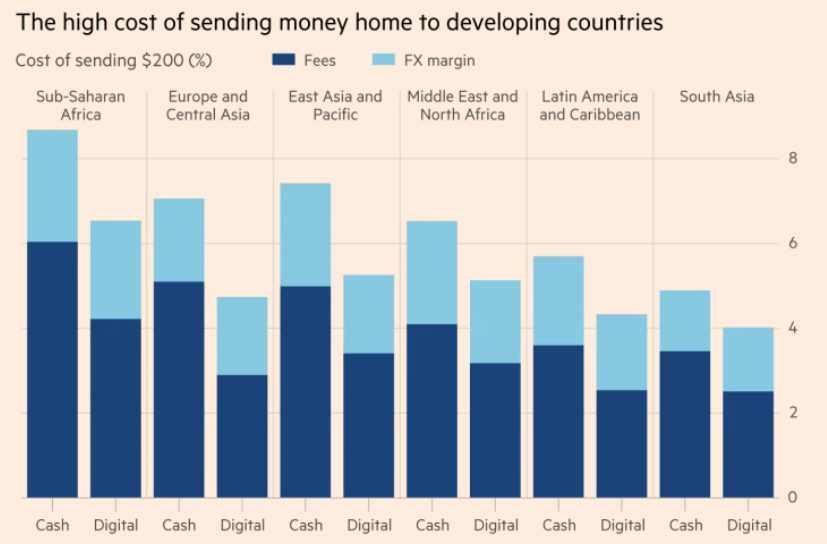

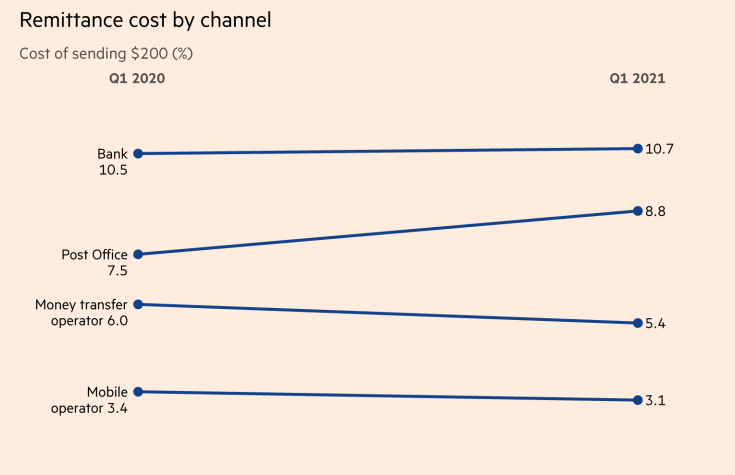

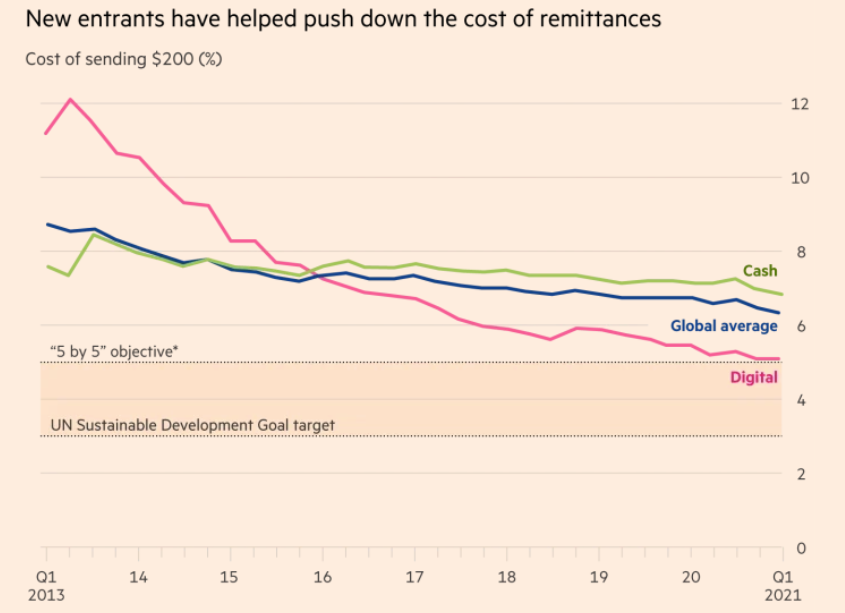

According to the World Bank, the bank confirms there has been a drop in global average charge around 9 per cent in 2011 to 6.4 per cent today for a cross-border transfer of $200. Therefore, G8 adopted a target in 2009, achieved by measuring as an average weighted for the value of transactions. Furthermore, the tech disruption of global payments is something to celebrate stated by World Bank.

Mayada Elzoghbi, a managing director of the Center for Financial Inclusion, stated that the target for 2030 is 3 per cent or below is "within reach". However, correspondent banks are dragging the anchor, and on average, they charge almost 11 per cent for a $200 switch. Money transfer operators have entered the market with affordable services. Also, mobile phone services cost two-thirds less than banks.

Lifeline for the developing world-Remittance

However, the developing countries benefit from lower costs if the sum increases, so the recipients there can invest in healthcare and education. The remittance in 2019 was worth $548bn, which was slightly more than the entirety of foreign direct investment. But the contribution from the governments to development spending in most wealthy countries is relatively puny. The report revealed that in Somalia, Lebanon, and Tonga, remittances are equivalent to more than a third of gross domestic product.

The World Bank predicted that remittances would fall sharply in the pandemic due to the seizing up of transport routes and migrant workers lack of work. But payments fell only by 1.6 percent. According to some economists, the migrants focused on remitting money home by sacrificing their welfare. Lockdowns accelerated cash onto formal and regulated platforms. Governments released anti-money laundering controls which made it easier for workers to register digital accounts.

Tiny increments equal to vast totals

Technology can overcome financial exclusion in developing countries where mobile phone penetration is high. Mobile transfer services have proved to be an aid by lowering the cost of money to the unbanked. Many fintech is picking off valuable payment corridors without offering a full global service. Observations say that banks and traditional money agents struggled to compete with the expectations of comprehensive customer service. Payments is a business where banks, except a few prominent players, depend on specialist service providers and network companies to move customers money around. Lenders will remain at the heart of the system for accepting deposits and making credit advances. Most of the new entrants do not want to shoulder the regulatory capital costs, and as a result, it reduces the reach of the banks. Furthermore, it triggered a race among payment businesses to bulk up capital-light payments.

Why do you consider becoming an International Money Transfer Operator today?

We at RemitAll Software have been focusing on the Remittance Business enablement. RemitAll have allowed businesses of all sizes, be it a high-street kiosk or an established Bank, to kick-start their remittance operations. Hence no matter where your business currently stands, our customised solution ensures safe money transactions worldwide. We provide that you don't lose your identity; Hence, RemitAll is fundamentally a white label solution that allows you to reach out to your customers with your brand. Hence, we deploy your brand website with login and money transfer features ably supported by iOS and Android applications.

To know more about how you can use the RemitAll software in your ecosystem; Please click here to provide us with your contact details, and we will call you back.

Wrap up

Sound risk management principles apply to the entire spectrum of risks facing a bank. Similarly, banks are required to have a thorough understanding of the inherent money laundering risks present in their customer base, product offerings, delivery channels, and service offerings. As a key success factor, banks are expected to identify the applicable risks in their correspondent relationships and implement internal controls to mitigate those risks, including having effective KYC processes.

So RemitAll Software is a safe and reliable technology that helps you to manage your remittance operations. It has clouds that safeguards your money transfer business against money laundering and terrorist funding activities. We have created technology to enhance your business network. Click on this link to know more about us https://www.remitall.co.uk.

Reading time 3:00 Minutes

Irene Asha Tirkey

Irene has completed her post-graduation in Integrated Marketing Communication from Calcutta Media Institute, Kolkata, India. Her key areas are blogging and content writing. She is in this industry for three years. Her interest areas include travelling listening to music, and painting.

Categories

Shifting Towards Digital Spell the End of Agents in Remittance. Yes or No?

May 20-2 Minutes 10 Seconds

Five Mantras For Digital Payments And User Friendly For Your Customers

May 21-2 Minutes 30 Seconds

Impact Of Remittance In Migration And Rural Development

May 27-2 Minutes 10 Seconds