Sandipan Deb

Sandipan DebJuly 13- 3:00 Minutes

Reimagining Remittances: A People-Centric Approach in Africa

It is common knowledge that laws and regulations are different based on which country you are in. And if you ever tried to transfer money outside of your country, you might have faced some obstacles or had to jump through different loops to do so. This is because each country has their state of affairs for remittances in the different countries.

Different countries have different rules and laws about what kind of companies can operate a money-transfer business. Maybe only fully licensed banks or FinTechs? or there may be laws in place about the maximum amount of a single transaction. There may be laws regarding what identifications can be accepted for remittance senders and receivers. Or the kind of bank account you must have to acquire and hold foreign currency. There even may be laws regarding what you can spend your money remittance money after receiving it.

What should be a simple act of sending your own money back home to your family can become a stressful process for migrants who have moved abroad to pursue a better life. Organisations like the Swedish International Development Cooperation Agency (SIDA) and the United Nations Capital Development Fund (UNCDF) are collaborating with various regulators to harmonise the many rules governing remittances. The goal behind this collaboration is to create comprehensive frameworks to support the flow of remittance.

The Prevailing Systems and Their Impact

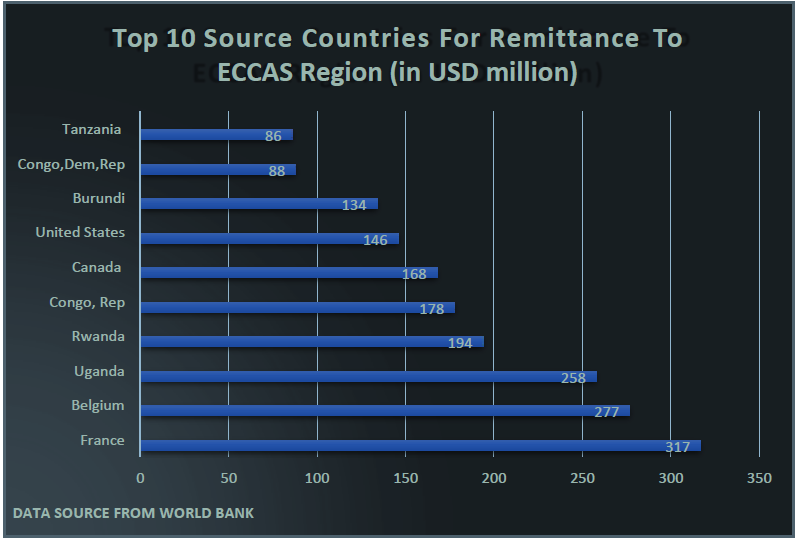

UNCDF and SIDA have started their work in Africa, one of the most important international remittance markets. They recently signed agreements with the continent’s two economic communities, IGAD (the Intergovernmental Authority on Development) and ECCAS (the Economic Community of Central African States).

According to the official World Bank statistics, the IGAD and ECCAS member states collectively received nearly $9 billion in remittances in 2019. This figure certainly does not show an accurate picture since many migrants rely on informal channels rather than navigate through the formal channel’s complex rules.

Today many people live and work outside their home countries to better provide for their families. But when a fluid labour market collides with a stringent financial system, the people suffer the consequences. The clutter of outdated regulations affects the migrants directly, meaning they cannot save, use or send their own money without risk or hassle. Lawmakers in various countries need to acknowledge this situation with a sense of urgency.

For millions of households throughout the developing world, remittances are not just a lifeline that keeps them from falling into poverty. Also, remittances are the foundation for their long-term goals like buying a new home, starting or expanding their business or providing higher education for their children. Almost all UN’s Sustainable Development Goals acknowledge the critical role remittances play in reducing poverty and promoting progress on various fronts.

Most of our attention seems focused on technology-empowered digital solutions for cross-border payments. Fintech has made international remittance affordable and accessible for many, but all the Fintech innovations will have limitations if the policies are not favourable. There are some things only lawmakers can do. Lawmakers must craft policy frameworks that promote their region’s household resilience while protecting the financial system’s integrity.

Opportunities Ahead

Most of the African migration stay within the continent between neighbouring countries. This presents a unique opportunity for African regional economic communities to revise the rule books that rewrite them in a more favourable way for their people. But this does not mean that such efforts should not be pursued for remittance corridors in other regions, for example, Asia to Africa or Europe to Africa.

The current collaboration between IGAD and ECCAS with SIDA and UNCDF is ideal for growth. They can build on past examples of African leadership, including the international payment settlement infrastructure in the Southern African Development Community and the harmonization of the East African Payment System. Another past example that comes to mind is the West African Monetary Zone Payments System Development Project which was signed on 9th Nov 2010.

UNCDF has a long history of delivering technical assistance and financing to the least developed countries in the world. And now, they are focused on a 360-degree global effort to reimagine remittances as a gateway product to create financial inclusion for migrant families in Africa. UNCDF and SIDA’s work with the African Union, the regional economic communities, member states and the joint Labour Migration Programme for Africa is towards improving migration policies and governance. They are actively trying to promote migrant’s rights and labour mobility in the African continent.

Conclusion

Remittance is a lifeline for many households in developing countries. While Fintech’s technology-driven solutions have contributed significantly to financial inclusion, much remains to be done on the policy maker’s part. This collaboration with UNCDF and SIDA and their partnership with regional economic communities are focused on promoting better financial governance for migrants in the African continent. Fewer obstacles and a people-centric approach in the formal financial system is the ultimate goal behind this collaboration.

Why choose us?

Remitall Software is a safe and reliable technology that helps you to manage your remittance operations. We take full responsibility for a hassle free experience to enhance your customer’s cross border money transfer requirements. Our technology enabled money transfer system is a blend services to improve your business network.

Reading time 3:00 Minutes

Sandipan Deb

Sandipan has completed his graduation in Media Science from NSHM Knowledge Campus, Kolkata, India. He is in the industry for two years. His key areas are content writing and digital marketing.

Categories

Shifting Towards Digital Spell the End of Agents in Remittance. Yes or No?

May 20-2 Minutes 10 Seconds

Five Mantras For Digital Payments And User Friendly For Your Customers

May 21-2 Minutes 30 Seconds

Impact Of Remittance In Migration And Rural Development

May 27-2 Minutes 10 Seconds