Irene Asha Tirkey

Irene Asha TirkeyAug 13- 3:00 Minutes

Remittances processed via mobile money increases by 65 percent in 2020

The unexpected resilience of remittance flows during the COVID-19 crisis highlights the importance of the timely availability of data. It overtakes foreign direct investment and official development assistance in low- and middle-income countries, but remittances can no longer be ignored as minor changes. Countries need to collect better data on remittances regarding frequency, timely reporting, and granularity.

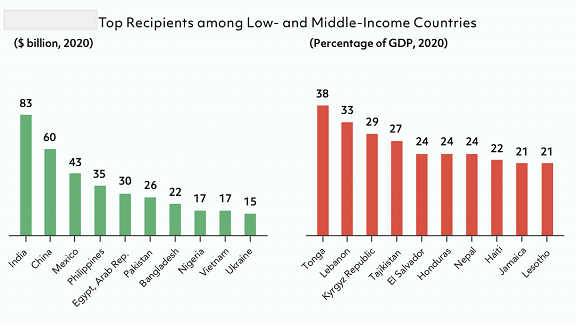

Remittance flows have proved to be resilient during the COVID-19 crisis

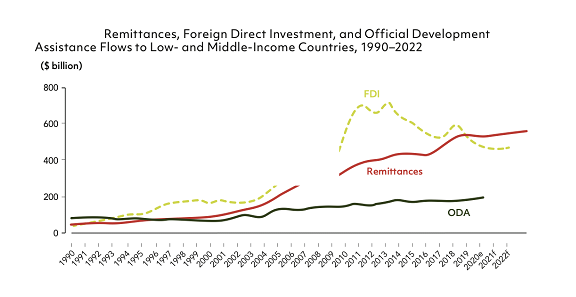

Remittance flows have proved to be resilient during the COVID-19 crisis. In 2020, remittance flowed to low- and middle-income countries (LMICs) reached $540 billion. The decline was smaller than the predictions published in April and October 2020 reported by World Bank.

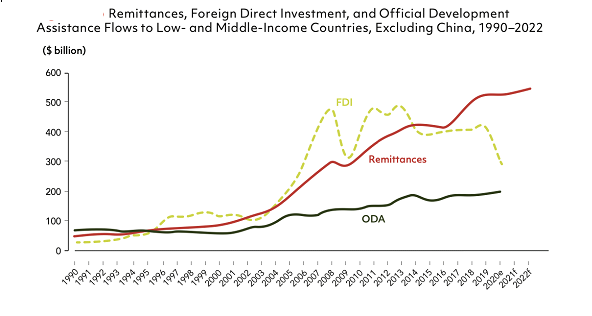

Thus, the gap between remittances and FDI widened further. Now the remittances have gained the spotlight as a consumption smoothing mechanism in developing countries. According to the report, FDI flows to LMICs declined by over 30 per cent in 2020. As a result, remittance flows to LMICs other than China surpassed the sum of FDI and official development assistance (ODA) in 2020.

Source: World Bank-KNOMAD (The Global Knowledge Partnership on Migration and Development)

Source: World Bank-KNOMAD (The Global Knowledge Partnership on Migration and Development)

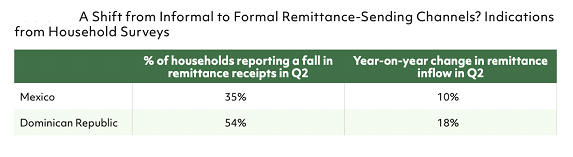

A shift from Informal to Formal Remittance-Sending Channels

The remittances industry has participated in the rapid acceleration of digitalisation. It was observed in multiple dimensions of firms’ and house- holds’ reactions to the COVID 19 crisis. The remittance flow increased from June 2020 through digital channels, especially for migrants with access to bank accounts and credit cards. Many leading money transfer operators reported double-digit growth in their digital services. So there was a sharp fall in their cash remittance services. The switch from cash to digital channels seems to have continued throughout 2020. Recent data showed that cross-border remittances processed via mobile money increased by 65 per cent in 2020.

Some reports revealed a broad shift from informal to formal channels in 2020 after digital remittances came into the market. Hence proving that digital remittances are better recorded than cash remittances. The true size of remittances includes formal and informal flows. However, the extent of the impact of COVID-19 on informal flows is still unclear.

Source: World Bank, COVID-19 High Frequency Monitoring Dashboard; IMF Balance of Payments Statistics.

Outlook for 2021-2022

In 2021 and 2022, economies worldwide are expected to rebound further(IMF 2021, Wolf 2021). Now, the low- and middle-income countries are pacing their performance with the developed countries. The incomes and employment of foreign-born workers help recover, increasing remittance flows to LMICs. The number of COVID-19-induced new poor in 2020 is likely to have risen to between 119 to 124 million. Thus, families in low- and middle-income countries need more support from migrant relatives overseas.

Based on recent trends in remittance flows, there is an assumption that the international migrant stock will not change much in the near term. The economic growth will be stronger this year, and remittance flows to LMICs are expected to increase by 2.6 per cent to $553 billion in 2021 and by 2.2 per cent to $565 billion in 2022.

Source: World Bank-KNOMAD staff.

Policy issues

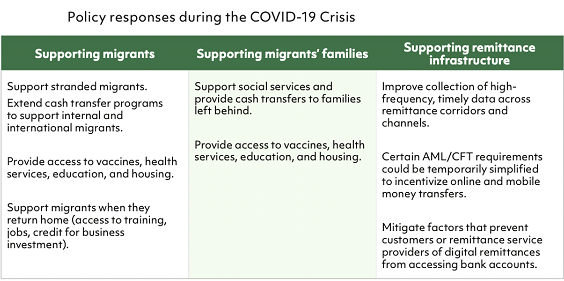

In World Bank studies (2020a and 2020b), public policy responses were discussed to support migrants and their families and keep remittances flowing during the crisis. There has been progress in some areas, for example, a few host countries have included migrants in cash transfer programs and vaccination programs.

Remittance costs across many African corridors and small islands in the Pacific remain above 10 per cent. Intraregional migrants in Sub-Saharan Africa comprise over two-thirds of all international migration from the region. Yet intraregional remittance costs are very high in the region due to the low volumes of formal flows.

Source: World Bank 2020b.

Conclusion

It is not the first time that remittance flows have proved resilient during a crisis. The same thing was observed in the aftermath of the global financial crisis. Remittances often rise in the recipient country's financial crisis or natural disasters (Ratha 2009; World Bank 2010). Remittances have provided a lifeline for families back home struggling with the loss of income and pandemic induced economic slowdown. Therefore it became an important consumption smoothing mechanism for the recipient households.

Do you want to start your money transfer operator business?

With RemitAll Software, you can remit worldwide. We take full responsibility for fuss-free transactions. Our compliance safeguards each transfer across every channel without facing any obstacles. A goal is to provide advanced technology without compromising security, quality and innovation for your clients. Connect with us by clicking on this link https://www.remitall.co.uk.

Reading time 3:00 Minutes

Irene Asha Tirkey

Irene has completed her post-graduation in Integrated Marketing Communication from Calcutta Media Institute, Kolkata, India. Her key areas are blogging and content writing. She is in this industry for three years. Her interest areas include travelling listening to music, and painting.

Categories

Shifting Towards Digital Spell the End of Agents in Remittance. Yes or No?

May 20-2 Minutes 10 Seconds

Five Mantras For Digital Payments And User Friendly For Your Customers

May 21-2 Minutes 30 Seconds

Impact Of Remittance In Migration And Rural Development

May 27-2 Minutes 10 Seconds