Irene Asha Tirkey

Irene Asha TirkeyJune 30- 3:00 Minutes

The Anti-Money-Laundering in Emerging Market Banks

In recent years, Anti-Money Laundering (AML) compliance requirements have marked increased cost and complexity to banks globally. While many of these regulatory changes have increased financial system resilience and helped battle financial crime. They have also put increased pressure on correspondent banking relationships and cross border financial networks. These networks make trade possible, support remittances, and facilitate foreign currency settlements.

Developments Around The AML And KYC Space

Money launderers target younger bank customers in their schemes. A recent study found that victims from the young group were accounted for more than 40 per cent of money mules, with a 5 per cent increase from 2019. Fraudsters typically exploit health crisis-related economic anxieties by offering potential mules a cut of the transferred funds. So they are dishonest about their plan to use the funds for and often threaten violence against those who try to back out of these schemes.

Oversight agencies are cracking down on banks with substandard AML procedures. More than $6.8 billion in compliance violation fine were issued to 28 financial institutions (FIs) across 14 countries in 2020. The largest single penalty was given to an Australian which was fined for $900 million. The fine was for the failure to report more than 19 million cross-border transactions over numerous years. Authorities said that some of these payments were allegedly linked to human trafficking operations in the Philippines.

The record-setting compliance total in 2020 could be a drop in the bucket compared to 2021. However, oversight agencies in the United States imposed $200 million in fines in the first two months of 2021, putting the year on pace to top 2020 by a wide margin. Most of the new fines result from the Anti-Money Laundering Act (AML Act) of 2020, which builds upon the Bank Secrecy Act of 1970. It included antique dealers and virtual currency marketplaces and gives law enforcement new tools to crack down on money laundering.

Risks encountered by banks

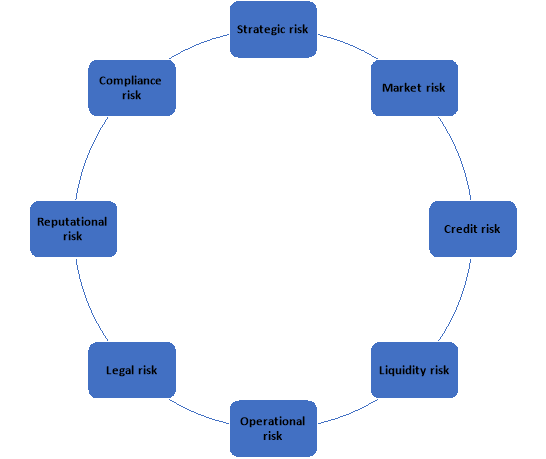

The term "risk" can be used for an opportunity or threat. But here, the risk is considered a threat. The principles of sound risk management apply to the entire spectrum of risks facing a financial institution. It includes business/strategic, market, credit, liquidity, operational, legal, reputational compliance risk and many more. Each of which is described as follows:

Business/Strategic risk= is the risk that affects or creates an organization's business strategy and strategic objectives.

Market risk= is the risk to a bank's financial condition resulting from adverse movements in market rates or prices, such as interest rates (for example, interest rate risk), foreign exchange rates, or equity prices.

Credit risk= arises from the potential that a borrower or counterparty will fail to perform on an obligation.

Liquidity risk= is the potential that an institution will be unable to meet its obligations. As they come due because of insufficient funds or an inability to liquidate assets or obtain adequate funding. In some cases, due to lowered market prices because of inadequate market depth or market disruptions, the institution does not meet its obligations.

Operational risk= arises from inadequate or failed internal processes, people, systems, or external events. Examples include inadequate information systems, operational execution problems, breaches in internal controls, fraud, or unforeseen external catastrophes that result in unexpected losses.

Legal risk= arises from the potential that are unenforceable contracts, lawsuits, or adverse judgments can disrupt. It can negatively affect the operations or condition of a banking organization.

Reputational risk= is the potential for negative publicity regarding an institution's business practices, whether true or not. It will cause a decline in the customer base, costly litigation, or revenue reductions.

-

Compliance risk= is exposure to legal penalties, financial forfeiture and material loss. An organization faces when it fails to act by the industry laws and regulations and internal policies or prescribed best practices.

Establishing a Sound Financial Institution Risk Management Framework

Taking risk is fundamental to the business of banking. Therefore managing the risks is critical to profitable and sustainable banking. Establishing a solid risk management framework for the range of risks encountered by a bank is essential for its safe and sound operation. A formal risk management program creates the framework for identifying, measuring, monitoring, reporting, and ultimately addressing risks.

A robust risk management framework sets the foundation for establishing an `AML program. Regardless of size and complexity, a bank must have adequate risk management programs designed for the organization's products, services, customers and overall risk profile. An adequate risk management frameworks can vary considerable based on the bank's business strategy, markets, and risk profile. However, their effectiveness ultimately judges them in managing risk across all a bank's operations.

Essential of a Sound AML program

A sound AML/CFT program is based on a complete understanding of the risks faced by the financial institution, relevant regulatory requirements, regulatory guidance, plus the potential impact of noncompliance. An AML program must incorporate all national needs and expectations.

Using best AML risk management practices will enable respondent banks to meet the expectations of correspondent banks that settle offshore transactions in U.S. dollars and euros. Furthermore, it will improve their ability to retain and continue providing cross-border banking services to their clients. A sound AML program will minimize the bank’s exposure to regulatory sanctions, penalties, and associated reputational risks.

As institutions develop more robust AML programs, ongoing investment can become an operational challenge as resource allocation for AML compliance typically increases. So enhancing AML programs to ensure continued cross-border banking services are available to clients. However, the bank remains connected to the global financial system by meeting international or other standards.

Wrap up

Sound risk management principles apply to the entire spectrum of risks facing a bank. Similarly, banks are required to have a thorough understanding of the inherent money laundering risks present in their customer base, product offerings, delivery channels, and service offerings. As a key success factor, banks are expected to identify the applicable risks in their correspondent relationships and implement internal controls to mitigate those risks, including having effective KYC processes.

So RemitAll Software is a safe and reliable technology that helps you to manage your remittance operations. It has clouds that safeguards your money transfer business against money laundering and terrorist funding activities. We have created technology to enhance your business network. Click on this link to know more about us https://www.remitall.co.uk.

Reading time 3:00 Minutes

Irene Asha Tirkey

Irene has completed her post-graduation in Integrated Marketing Communication from Calcutta Media Institute, Kolkata, India. Her key areas are blogging and content writing. She is in this industry for three years. Her interest areas include travelling listening to music, and painting.

Categories

Shifting Towards Digital Spell the End of Agents in Remittance. Yes or No?

May 20-2 Minutes 10 Seconds

Five Mantras For Digital Payments And User Friendly For Your Customers

May 21-2 Minutes 30 Seconds

Impact Of Remittance In Migration And Rural Development

May 27-2 Minutes 10 Seconds