Irene Asha Tirkey

Irene Asha TirkeyAug 25- 3:00 Minutes

The technology of central bank digital currency

The economy is in the middle of a technological revolution. This revolution considers the digitalisation of the financial system and even the design of money itself. Combining new digital technologies and greater online activity allows vast volumes of data to be collected, managed and telecommunicated. Surprisingly it has resulted in robust, hyper-scalable applications that have disrupted entire industries. The market welcomes new players in the digital economy to provide these services. Covid-19 pandemic may have further accelerated the pace of digital change.

Payments are attractive for digital disrupters because they are relatively less capital-intensive than other financial services and generate valuable cross-selling information. Perhaps it is no surprise that a concrete burst of digital innovation in payment industry has opened opportunities for fintech start-ups, big techs and incumbents.

“Central banks and payments in the digital era”

“Digital cash” is in the news lately, including central bank digital currencies, or CBDCs. Therefore central bank digital currencies or CBDCs uses an electronic record to represent the virtual form of a fiat currency of a particular nation. A CBDC is centralised, and it is issued and regulated by the competent monetary authority of the country.

There are two types of central bank digital currencies, namely wholesale realm and retail space. Therefore wholesale realm stands for payments between financial institutions and large commercial parties. Digital central bank money for wholesale purposes already exists in the form of central bank reserves. Notably, privately issued wholesale digital currencies, also called utility tokens or wholesale stable coins, are not separate currencies per se. They still depend on central banks for the finality of clearing and settlement. Likewise the stable coin, they still have an “umbilical cord” connecting them to the financial system.

While the other type of digital currency is the retail space. Retail digital currencies could be used in daily transactions by households and businesses. The BIS has surveyed central banks around the world on their engagement with CBDCs. BIS Paper stated that a full 86% of 65 respondent central banks are now doing some research or experimentation. Some are working primarily on the wholesale side, and some on retail, but the rest and largest number are looking on both. Increasingly, central banks are now moving beyond research towards actual pilots. Since 2020, there has been a live CBDC with the Sand Dollar project in the Bahamas. Likewise, the Boston Fed is working with the MIT Digital Currency Initiative on retail CBDC research that will be open source for all to review.

Source: BIS Papers, no 114, January 2021.

“Money is memory”

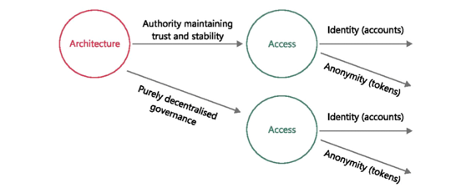

While Narayana Kocherlakota, monetary theorist and a former president of the Federal Reserve Bank of Minneapolis, argued in his famous paper 1998 that “money is memory”. Money is a freely accessible device that records who owes what to whom rather than substituting it for a complex web of bilateral IOUs.

Money is the economy’s memory, leading to two forks in the road to design digital money. In payments parlance, it means ensuring the integrity and safety of the payment system and the finality of payments. He also questions the roles of a central intermediary versus a decentralised governance system. Simultaneously, access to the information with appropriate safeguards in place to protect privacy is vital. In other words, proper identification and confidentiality in the payment system should be established.

Source : BIS Quarterly Review, March 2020

Hybrid CBDC architectures

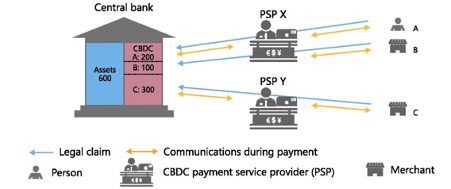

Money has always been a social convention involving both the private sector and the central bank or other public authorities. In contrast, money is an instance of a public-private partnership. CBDCs realised and designed to preserve the two-tiered financial system as a public-private partnership. According to the user's perspective, a successful retail CBDC demands a resilient and inclusive digital complement to physical cash without precluding a vital role for the private sector.

The BIS research scopes out how two-tier “Hybrid” and “Intermediated” CBDC architectures can involve the private sector as the default payments operator. But with the central bank's support, they will operate a backup infrastructure to provide additional resilience. It will benefit the users to pay with a CBDC just as today, with a debit card, online banking tool or smartphone-based app, all operated by a bank or other private sector payment provider.

However, the CBDC itself would be a cash-like claim on the central bank. In this way, the central bank can evade the operational tasks of opening accounts and administering payments for users. At the same time, the private sector intermediaries will continue to perform retail payment services without balance sheet concerns. Further, these architectures also allow the central bank to operate backup systems if the private sector runs into technical outages.

Source : BIS Quarterly Review, March 2020

Conclusion

Developing CBDC comes with a host of technological, legal and economic issues that vouch for careful examination before issuance. Central banks stand as the guardians of stability to proceed carefully, methodically and in line with their mandates. Now CBDCs have a positive impact on payment options that coexist with private sector electronic payment systems and cash. Few issues require like “digital dollarisation“ and the potential role of CBDCs in enhancing cross-border payments. The BIS extend its supports by ensuring that central banks can continue learning from one another and cooperate on key issues in design. Therefore central banks can work together to support digital money get ready for the economy of the future.

Source: BIS Papers, no 114, January 2021.

This article is brought you by RemitAll Software a technology to enhance your business network. Do you want to start with a money transfer business? Then RemitAll Software is the best choice to opt for hassle-free remittance solutions for all dimensions of business. We assure you of your growth and return your business right on track with the money remittance application. Get connected with us by clicking on this link https://www.remitall.co.uk

Reading time 3:00 Minutes

Irene Asha Tirkey

Irene has completed her post-graduation in Integrated Marketing Communication from Calcutta Media Institute, Kolkata, India. Her key areas are blogging and content writing. She is in this industry for three years. Her interest areas include travelling listening to music, and painting.

Categories

Shifting Towards Digital Spell the End of Agents in Remittance. Yes or No?

May 20-2 Minutes 10 Seconds

Five Mantras For Digital Payments And User Friendly For Your Customers

May 21-2 Minutes 30 Seconds

Impact Of Remittance In Migration And Rural Development

May 27-2 Minutes 10 Seconds